This is the only politician speaking on behalf of the average Joe. Way to go!

http://4closurefraud.org/2011/11/30/elijah-cummings-oversight-committee-democrats-urge-fhfa-director-to-produce-documents-on-principal-reduction/

An informational blog pertaining to foreclosure law and foreclosure defense practice.

© Copyright 2015 Law Offices of Robert E. Brown, P.C. All Rights Reserved.

Wednesday, November 30, 2011

Interview with Scott Olsen About His Injury from the Police Attack on Occupy Oakland (Video)

Wake up people! America as you know it is slowly changing right before our eyes!

http://4closurefraud.org/2011/11/30/interview-with-scott-olsen-about-his-injury-from-the-police-attack-on-occupy-oakland-video/

http://4closurefraud.org/2011/11/30/interview-with-scott-olsen-about-his-injury-from-the-police-attack-on-occupy-oakland-video/

Are loss-share lenders gouging us?

OneWest Bank got a GREAT deal from the FDIC also. Nothing like buying bad loans from the FDIC and having your down side limited! Hey, no problem the taxpayers will cover you!

http://4closurefraud.org/2011/11/30/fraudclosure-are-fdic-loss-share-lenders-gouging-us/

http://4closurefraud.org/2011/11/30/fraudclosure-are-fdic-loss-share-lenders-gouging-us/

Employment and Income Fraud on the Rise

No surprise here. As credit tightens it will get worse.

http://www.dsnews.com/articles/print-view/employment-income-fraud-on-rise-2011-11-29

http://www.dsnews.com/articles/print-view/employment-income-fraud-on-rise-2011-11-29

Adam Levitin | HARP’s Dirty Little Secret: Most HARP Refis are of Positive Equity Mortgages

Wait, that can't be true. A Government program created to help underwater borrowers refinance helps very few of them . . . . . . . Surprise!!!!!!!!!!

http://4closurefraud.org/2011/11/30/adam-levitin-harps-dirty-little-secret-most-harp-refis-are-of-positive-equity-mortgages/

http://4closurefraud.org/2011/11/30/adam-levitin-harps-dirty-little-secret-most-harp-refis-are-of-positive-equity-mortgages/

DO You Have A Mortgage With BAC Home Loans Servicing?

If the lender foreclosing on your property is BAC HOME LOANS SERVICING. Please contact our office at jbrancato@robertbrownlaw.com for some very important information.

Police, Movers Refuse to Evict 103-Year-Old Woman from Foreclosed Home of 53 Years

I guess if the bank wants to evict this woman they can send an executive to do it!

http://4closurefraud.org/2011/11/30/police-movers-refuse-to-evict-103-year-old-woman-from-foreclosed-home-of-53-years/

http://4closurefraud.org/2011/11/30/police-movers-refuse-to-evict-103-year-old-woman-from-foreclosed-home-of-53-years/

Robo-signer Whisleblower Found Dead in Nevada

The Law Offices of Robert E. Brown, P.C.

A notary public who signed tens of thousands of false documents in a massive foreclosure scam before blowing the whistle on the scandal has been found dead in her Las Vegas home.

Full Story: http://4closurefraud.org

Banks May Have Illegally Foreclosed on Members of the Military

The Law Offices of Robert E. Brown, P.C.

Ten leading US lenders may have unlawfully foreclosed on the mortgages of nearly 5,000 active-duty members of the US military in recent years, according to data released by a federal regulator.

Full Story: http://www.truth-out.org

Tuesday, November 29, 2011

Secret Fed Loans Gave Banks $13 Billion

The Law Offices of Robert E. Brown

The Federal Reserve and the big banks fought for more than two years to keep details of the largest bailout in U.S. history a secret. Now, the rest of the world can see what it was missing.

The Full story can be found here: http://www.bloomberg.com

Monday, November 28, 2011

Mr. Romney on Foreclosures

This guy knows NOTHING about finance OR real estate. Which means he knows NOTHING about foreclosures. And he wants to become president. Good luck!

http://www.nytimes.com/2011/11/27/opinion/sunday/mr-romney-on-foreclosures.html?_r=1

http://www.nytimes.com/2011/11/27/opinion/sunday/mr-romney-on-foreclosures.html?_r=1

Baum fall throws NY foreclosures a curve

And so the unwinding begins. . . . . . .

http://www.nypost.com/p/news/business/baum_fall_throws_ny_foreclosures_Z3Twy2tQIrIc4Qr7WggHtL

http://www.nypost.com/p/news/business/baum_fall_throws_ny_foreclosures_Z3Twy2tQIrIc4Qr7WggHtL

Friday, November 25, 2011

Baum abandons foreclosure case

We may begin to see even more of these cases!

http://stopforeclosurefraud.com/2011/11/10/u-s-bank-n-a-v-solorin-nysc-dismisses-complaint-abandoned-steven-j-baum-pc-plaintiff-attorney-affirmation/?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+ForeclosureFraudByDinsfla+%28FORECLOSURE+FRAUD+%7C+by+DinSFLA%29

http://stopforeclosurefraud.com/2011/11/10/u-s-bank-n-a-v-solorin-nysc-dismisses-complaint-abandoned-steven-j-baum-pc-plaintiff-attorney-affirmation/?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+ForeclosureFraudByDinsfla+%28FORECLOSURE+FRAUD+%7C+by+DinSFLA%29

Desert Underwater Part 5: Who Owns Your Home?

This problem will be the last to be addressed. . .unfortunately.

http://4closurefraud.org/2011/11/25/desert-underwater-part-5-who-owns-your-home/

http://4closurefraud.org/2011/11/25/desert-underwater-part-5-who-owns-your-home/

Foreclosure firm’s collapse could delay cases statewide

ALL of these "foreclosure mills" should be investigated ASAP!

http://stopforeclosurefraud.com/2011/11/23/foreclosure-firms-collapse-could-delay-cases-statewide/?utm_source=feedburner&utm_medium=twitter&utm_campaign=Feed%3A+ForeclosureFraudByDinsfla+%28FORECLOSURE+FRAUD+%7C+by+DinSFLA%29

http://stopforeclosurefraud.com/2011/11/23/foreclosure-firms-collapse-could-delay-cases-statewide/?utm_source=feedburner&utm_medium=twitter&utm_campaign=Feed%3A+ForeclosureFraudByDinsfla+%28FORECLOSURE+FRAUD+%7C+by+DinSFLA%29

Pols Rally for Foreclosure Assistance Funding

These not-for-profits should get all the money they need. This foreclosure crisis is certainly NOT going to go away anytime soon. Kudos to Staten Island Legal Services!

http://www.politickerny.com/2011/11/21/pols-rally-for-foreclosure-assistance-funding/

http://www.politickerny.com/2011/11/21/pols-rally-for-foreclosure-assistance-funding/

Cummings Calls for Unredacted Copies of “Engagement Letters” Between Mortgage Servicing Companies and Private Consultants

ALL of our elected officials need to jump on this !!!!

http://4closurefraud.org/2011/11/23/cummings-calls-for-unredacted-copies-of-engagement-letters-between-mortgage-servicing-companies-and-private-consultants/

http://4closurefraud.org/2011/11/23/cummings-calls-for-unredacted-copies-of-engagement-letters-between-mortgage-servicing-companies-and-private-consultants/

Whistleblowers ignored, punished by lenders, dozens of former employees say

So let me get this straight. You hire internal fraud investigators and when they find something you believe shouldn't be reported you threaten, harass and fire these people? I don't get it!!!!!

http://www.iwatchnews.org/2011/11/22/7461/whistleblowers-ignored-punished-lenders-dozens-former-employees-say

http://www.iwatchnews.org/2011/11/22/7461/whistleblowers-ignored-punished-lenders-dozens-former-employees-say

Robo-Signing Problems on Foreclosure Documents

I have to ask this again. . . why hasn't anyone gone to prison yet???

http://4closurefraud.org/2011/11/25/desert-underwater-part-3-robo-signing-problems-on-foreclosure-documents/

http://4closurefraud.org/2011/11/25/desert-underwater-part-3-robo-signing-problems-on-foreclosure-documents/

Tuesday, November 22, 2011

The Law Offices of Robert E. Brown, P.C. Welcomes the Addition of Attorney Michael A. Mazalatis

The Law Offices of Robert E. Brown, P.C. announces the addition of attorney Michael A. Mazalatis to the law firm.

Member, State Bar of New Jersey (November 2010 - Present)

Member, State Bar of New York (March 2011 – Present)

Admission, United States District Court for the District of New Jersey

Whom Do You Serve? UC Davis Protestors Pepper Sprayed for Sitting on the Ground

Absolutely disgusting!

http://4closurefraud.org/2011/11/21/whom-do-you-serve-uc-davis-protestors-pepper-sprayed-for-sitting-on-the-ground/

http://4closurefraud.org/2011/11/21/whom-do-you-serve-uc-davis-protestors-pepper-sprayed-for-sitting-on-the-ground/

Baum Firm Could Possibly Owe “Millions of Dollars” From Foreclosured Properties

I'm sure there are many parties seeking restitution from Baum. Better move on him now before there's nothing left.

http://stopforeclosurefraud.com/2011/11/21/baum-firm-could-possibly-owe-millions-of-dollars-from-foreclosured-properties/

http://stopforeclosurefraud.com/2011/11/21/baum-firm-could-possibly-owe-millions-of-dollars-from-foreclosured-properties/

Negative Equity: How Many Loans are Underwater in Your State?

As the real estate market continues to decline you may feel the only way out is a short sale or deed-in-lieu (of foreclosure). Take note that the banks will try to make you cover any of their losses. Be certain to hire an attorney that is familiar with deficiency judgments because the banks will most certainly come after you for any losses.

http://www.creditsesame.com/blog/negative-equity-how-many-loans-are-underwater-in-your-state/

http://www.creditsesame.com/blog/negative-equity-how-many-loans-are-underwater-in-your-state/

Lawmaker Questions If GSE Penalties Contributed to Foreclosure Abuses

So the Federal Housing Finance Agency(FHFA)knew about Robo-signing "years ago"?! And then assessed $150 million in fines against servicers for NOT pushing foreclosures through the system faster?!?!? I'm completely at a loss for words here.

http://www.dsnews.com/articles/lawmaker-questions-if-gse-penalties-contributed-to-foreclosure-abuses-2011-11-21

http://www.dsnews.com/articles/lawmaker-questions-if-gse-penalties-contributed-to-foreclosure-abuses-2011-11-21

Monday, November 21, 2011

After Arrest | Retired Police Captain Raymond Lewis Joins Occupy Wall Street (VIDEO)

Retired police captain gets arrested for the rights of others. N.Y.P.D. must realize THEY too are part of the 99%.

http://4closurefraud.org/2011/11/21/after-arrest-retired-police-captain-raymond-lewis-joins-occupy-wall-street-video/

http://4closurefraud.org/2011/11/21/after-arrest-retired-police-captain-raymond-lewis-joins-occupy-wall-street-video/

OUTRAGEOUS | Miriam Mendieta, Esq., Former Managing Partner of David J. Stern’s Fraud Factory to Lead Review of 4.5 Million Foreclosure Cases

As soon as the banks announced THEY would be the ones hiring the auditors you knew there would be a problem. They must really believe we're a bunch of idiots.

http://4closurefraud.org/2011/11/21/outrageous-miriam-mendieta-esq-former-managing-partner-of-david-j-sterns-fraud-factory-to-lead-review-of-4-5-million-foreclosure-cases/

http://4closurefraud.org/2011/11/21/outrageous-miriam-mendieta-esq-former-managing-partner-of-david-j-sterns-fraud-factory-to-lead-review-of-4-5-million-foreclosure-cases/

Baum law firm to close

He has no one to blame but himself.

http://www.bizjournals.com/buffalo/news/2011/11/21/baum-law-firm-to-close.html

http://www.bizjournals.com/buffalo/news/2011/11/21/baum-law-firm-to-close.html

Predatory Loan Test

You May Have a Predatory or Fraudulent Mortgage If:

•The closing took place in your home or place of business

•There was no physical closing

•You never signed any paperwork

•You never received all of your paperwork

•The mortgage broker promised or paid you to close

•You received no paperwork before the closing

•You were promised a fixed rate loan and then received an adjustable rate

•Your payment was higher than broker stated it would be

•You were told your payment included taxes and insurance

•You were told you needed to buy “life insurance” in order to be approved

•Your income was inflated

•You were approved for the loan based on the value of your home not on your income

•The mortgage broker increased the number of apartments on your application

•The broker added bank accounts you don’t have or inflated the balance in them

•The mortgage broker received an “extra” payment from the bank (known as a Y.S.P.)

•The mortgage broker earned more than what would be consider reasonable

•You refinanced multiple times (loan flipping)

•Broker promised to refinance you into a “better loan”

•Interest rate is higher than promised or incorrect

•Cash out promised is less than received

•Closing costs are higher than stated

•High closing costs

•Unearned or bogus fees paid to the bank or broker

•Payment to mortgage broker is higher than shown on closing statement (HUD)

•You were specifically targeted for a specific type of loan (more fees for broker)

•You were locked into the loan for a long period (or you had to pay a fee)

If you have any questions regarding your mortgage, predatory lending or how we can help you to fight back against foreclosure please feel to contact us.

Law Offices of Robert E. Brown, P.C.

2409 Richmond Rd., Staten Island, New York 10306

Phone: 718-979-9779 Email: jbrancato@robertbrownlaw.com

Attorney Advertising

•The closing took place in your home or place of business

•There was no physical closing

•You never signed any paperwork

•You never received all of your paperwork

•The mortgage broker promised or paid you to close

•You received no paperwork before the closing

•You were promised a fixed rate loan and then received an adjustable rate

•Your payment was higher than broker stated it would be

•You were told your payment included taxes and insurance

•You were told you needed to buy “life insurance” in order to be approved

•Your income was inflated

•You were approved for the loan based on the value of your home not on your income

•The mortgage broker increased the number of apartments on your application

•The broker added bank accounts you don’t have or inflated the balance in them

•The mortgage broker received an “extra” payment from the bank (known as a Y.S.P.)

•The mortgage broker earned more than what would be consider reasonable

•You refinanced multiple times (loan flipping)

•Broker promised to refinance you into a “better loan”

•Interest rate is higher than promised or incorrect

•Cash out promised is less than received

•Closing costs are higher than stated

•High closing costs

•Unearned or bogus fees paid to the bank or broker

•Payment to mortgage broker is higher than shown on closing statement (HUD)

•You were specifically targeted for a specific type of loan (more fees for broker)

•You were locked into the loan for a long period (or you had to pay a fee)

If you have any questions regarding your mortgage, predatory lending or how we can help you to fight back against foreclosure please feel to contact us.

Law Offices of Robert E. Brown, P.C.

2409 Richmond Rd., Staten Island, New York 10306

Phone: 718-979-9779 Email: jbrancato@robertbrownlaw.com

Attorney Advertising

Disparities in Mortgage Lending and Foreclosures

The Law Offices of Robert E. Brown, P.C.

“Lost Ground, 2011” is based on an analysis of 27 million mortgages made over a five-year period. Here are our top-line findings:

Disparities in Mortgage Lending and Foreclosures: Maps and Data

Executive Summary

The full article can be found here: responsiblelending.org

“Lost Ground, 2011” is based on an analysis of 27 million mortgages made over a five-year period. Here are our top-line findings:

The nation is not even halfway through the foreclosure crisis. 6.4 percent of mortgages made between 2004 and 2008 have ended in foreclosure, and an additional 8.3 percent are at immediate, serious risk.

Foreclosure patterns are strongly linked with patterns of risky lending. Foreclosure rates are consistently worse for borrowers who received high-risk loan products that were aggressively marketed before the housing crash.

The majority of people affected by foreclosures have been white families. However, borrowers of color are more than twice as likely to lose their home as white households.

Foreclosure Damage IndexDisparities in Mortgage Lending and Foreclosures: Maps and Data

Executive Summary

The full article can be found here: responsiblelending.org

Saturday, November 19, 2011

Breaking The Law… Again | ACLU, Florida Press Association, First Amendment Foundation Letter to Hillsborough County Chief Judge Menendez “Stop Blockin

AGAIN, the public is denied access to foreclosure hearings?? What the hell is going on in Florida??? Unbelievable!

http://4closurefraud.org/2011/11/18/breaking-the-law-again-aclu-florida-press-association-first-amendment-foundation-letter-to-hillsborough-county-chief-judge-menendez-stop-blocking-citizens-from-attending-foreclosure-court/

http://4closurefraud.org/2011/11/18/breaking-the-law-again-aclu-florida-press-association-first-amendment-foundation-letter-to-hillsborough-county-chief-judge-menendez-stop-blocking-citizens-from-attending-foreclosure-court/

Baum Weighs In After Uproar

Something tells me Baum will become an expert at throwing anyone he can under the bus to save his own skin. He has no one to blame but himself. Like I said - If I were a Baum employee I'd starting looking for a new job - yesterday!

http://www.nytimes.com/2011/11/19/opinion/nocera-baum-weighs-in-after-uproar.html?_r=2

http://www.nytimes.com/2011/11/19/opinion/nocera-baum-weighs-in-after-uproar.html?_r=2

Friday, November 18, 2011

Analysis: SEC targets low-level bankers, spares top execs

The SEC - A Toothless Dog on a Short Leash. Throw the little banker under the bus while the head bankster drives it away. Nice going!

http://stopforeclosurefraud.com/2011/11/15/analysis-sec-targets-low-level-bankers-spares-top-execs/?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+ForeclosureFraudByDinsfla+%28FORECLOSURE+FRAUD+%7C+by+DinSFLA%29

http://stopforeclosurefraud.com/2011/11/15/analysis-sec-targets-low-level-bankers-spares-top-execs/?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+ForeclosureFraudByDinsfla+%28FORECLOSURE+FRAUD+%7C+by+DinSFLA%29

SIGTARP, Google Crack Down on Mortgage Modification Scams

Sadly, many of these borrowers will be taken for a lot of money before they come and see us. Many times it is either too late or they've spent everything they have. You need to know who you're dealing with before spending your hard-earned cash.

http://www.americanbanker.com/issues/176_223/sigtarp-google-mortgages-modifications-1044136-1.html?ET=americanbanker:e8802:1903271a:&st=email&utm_source=editorial&utm_medium=email&utm_campaign=AB_Washington_Regulatory_111711

http://www.americanbanker.com/issues/176_223/sigtarp-google-mortgages-modifications-1044136-1.html?ET=americanbanker:e8802:1903271a:&st=email&utm_source=editorial&utm_medium=email&utm_campaign=AB_Washington_Regulatory_111711

Freddie Mac to securitize previously delinquent mortgages

So, I guess NO lessons have been learned??? Sounds like just another way to earn more revenue. I would like to know how the loans became "performing". More than likely the borrowers were pushed into shoddy loan mods or worse - repayment plans. That makes perfect business sense - push borrowers to become current and then securitize and peddle them as performing. I'm sure you can "buy" a good rating for the securitized loans and you're good to go! Great work guys!

http://4closurefraud.org/2011/11/17/just-when-you-thought-you-heard-it-all-freddie-mac-set-to-securitize-previously-delinquent-mortgages/

http://4closurefraud.org/2011/11/17/just-when-you-thought-you-heard-it-all-freddie-mac-set-to-securitize-previously-delinquent-mortgages/

Woman Gets Jail For Food-Stamp Fraud; Wall Street Fraudsters Get Bailouts

I guess the lesson here is if you're going to steal, you need to steal a LOT of money (like the bankers)! And then you won't go to prison. Great lesson to teach the kids.

http://4closurefraud.org/2011/11/18/matt-taibbi-woman-gets-jail-for-food-stamp-fraud-wall-street-fraudsters-get-bailouts/

http://4closurefraud.org/2011/11/18/matt-taibbi-woman-gets-jail-for-food-stamp-fraud-wall-street-fraudsters-get-bailouts/

Foreclosure mill getting peppered

Poor, poor Baum. The chickens are coming home to roost. With half of his revenue coming from the two giants (Fannie & Freddie) it won't be long before he'll begin to have a real cash flow problem. If I were a Baum employee I would start looking for another job. The writing is on the wall folks.

http://m.nypost.com/p/news/business/foreclosure_mill_getting_peppered_kiOTIVUoa2nNSftA2YwZKJ

http://m.nypost.com/p/news/business/foreclosure_mill_getting_peppered_kiOTIVUoa2nNSftA2YwZKJ

Thursday, November 17, 2011

Nevada Grand Jury Indicts Two in Alleged Robo-Signing Scheme

Full Story Click Here: The Wall Street Journal

Are You a Victim of Predatory Lending or Fraud?

Do you know the signs of a predatory loan? (Hint - think how your mortgage broker was paid). You may be a victim of predatory lending and not even know it! If you're in foreclosure one reason may be because of the type of loan you have. If you're not sure you have a predatory loan email us for a free copy of the Signs of Predatory Lending. If you have questions about predatory lending, fraud or foreclosures send us an email and we'll be happy to provide a free private consultation (by phone or email).

John Brancato, Loss Mitigation

jbrancato@robertbrownlaw.com

John Brancato, Loss Mitigation

jbrancato@robertbrownlaw.com

Wednesday, November 16, 2011

Are You a Victim of Predatory Lending or Fraud?

Do you know the signs of a predatory loan? (hint - think how your mortgage broker was paid). You may be a victim of predatory lending and not even know it! If you're in foreclosure one reason may be because of the type of loan you have. If you're not sure you have a predatory loan email us for a free copy of the Signs of Predatory Lending. If you have questions about predatory lending, fraud or foreclosures send us an email and we'll be happy to provide a free private consultation (by phone or email).

John Brancato, Loss Mitigation

Death Knell For ‘Robo-Signing’?

The Law Offices of Robert E. Brown, P.C.

Morgan Stanley agrees to end practice...

Full Story:

Financial Fraud Law

Morgan Stanley agrees to end practice...

Full Story:

Financial Fraud Law

Bank Excuses on Foreclosure Growing Stale

The Law Offices of Robert E. Brown, P.C.

"Bank of America got a bailout, and this is an outrage, how this man has been treated,” she said. “Hard-working, middle-class Americans are trying to make it, trying to refinance with your bank.”

Either bank officials show up in person, the justice said, or I’m going to order them “here in handcuffs.”

For Full Story:

Tuesday, November 15, 2011

A Coming Nightmare of Homeownership?

Too big to fail . . again?

Occupy Buffalo protesters picket at Baum law office

Too bad he wasn't there to witness that!

JUDGE DENNIS BLACKMON NAILS US BANK IN GEORGIA ON HAMP, WRONGFUL FORECLOSURE

Wow! If more judges had this same thought process banks wouldn't be so bold.

Court Order | Judge Rules Occupy Wall Street Protesters Can’t Camp in Zuccotti Park

What the police don't realize is that THEY are also the 99%!

http://4closurefraud.org/2011/11/15/court-order-judge-rules-occupy-wall-street-protesters-cant-camp-in-zuccotti-park/

Think You Have a Predatory Loan?

Do You Have Any Of These Violations On Your Mortgage?

Below you will find some of the results we have found after auditing our client’s mortgages:

Audited Results:

* Excessive fee charged to borrower

* Over compensation to mortgage broker

* Wrong lender foreclosing on borrower

* Borrower never received acceleration notice

* No HUD given to borrower at closing

* Mortgage broker over stated borrower’s income

* Mortgage broker added false bank account to borrower’s loan application

* Asset based lending

* Bait and switch. Borrower was switched at closing into an ARM loan

* No pre-closing documents – TIL, GFE, IOAF, Loan type, Broker’s fees

* Margin 7.125% (Adjustable rate loans only)

* TIL and Note payments do not match

* TIL does not clearly state mortgage payment

* Loan discount $ 9,315.00 – No benefit to borrower

* Mortgage broker never disclosed their additional fees

* Mortgage broker promised borrower a cash out of $76,000 if they closed the loan.

* Borrower received no note at the closing

* Borrower never signed closing documents. Broker “lifted” signatures from a previous loan.

* Mortgage broker did home closing without an attorney, notary or title company.

* Foreclosure filed during the 30 notice period

* Loan flipping. No benefit to borrower

* Closing costs ($75,966.65) higher than GFE ($47,377.15)

* $28,589.50 missing from closing (HUD)

* Hidden payment to mortgage by bank (YSP $17,402.16)

* Mortgage broker over stated borrower’s bank account by $80,400.00

* Borrower was charged for the presence of an attorney when no one presented them

* High cost loan

* APR higher

* Borrower never received cash out as shown on HUD

* Borrower received no documents at closing

* Dual tracking (lender started to foreclose while working on a modification)

* Borrower never served foreclosure documents

* Foreclosure illegally started

* Bank took payments from borrower and than foreclosed

* Process server falsified documents stating they served borrower when they did not.

* No pre-foreclosure documents given to borrower

* Foreclosure filed during the 30 day and 90 period.

* Real Estate broker, mortgage broker and attorney worked together to obtain financing and sell property to an unsuspecting borrower providing him with false and misleading information

while also giving inaccurate and deceptive information to the lender.

Below you will find some of the results we have found after auditing our client’s mortgages:

Audited Results:

* Excessive fee charged to borrower

* Over compensation to mortgage broker

* Wrong lender foreclosing on borrower

* Borrower never received acceleration notice

* No HUD given to borrower at closing

* Mortgage broker over stated borrower’s income

* Mortgage broker added false bank account to borrower’s loan application

* Asset based lending

* Bait and switch. Borrower was switched at closing into an ARM loan

* No pre-closing documents – TIL, GFE, IOAF, Loan type, Broker’s fees

* Margin 7.125% (Adjustable rate loans only)

* TIL and Note payments do not match

* TIL does not clearly state mortgage payment

* Loan discount $ 9,315.00 – No benefit to borrower

* Mortgage broker never disclosed their additional fees

* Mortgage broker promised borrower a cash out of $76,000 if they closed the loan.

* Borrower received no note at the closing

* Borrower never signed closing documents. Broker “lifted” signatures from a previous loan.

* Mortgage broker did home closing without an attorney, notary or title company.

* Foreclosure filed during the 30 notice period

* Loan flipping. No benefit to borrower

* Closing costs ($75,966.65) higher than GFE ($47,377.15)

* $28,589.50 missing from closing (HUD)

* Hidden payment to mortgage by bank (YSP $17,402.16)

* Mortgage broker over stated borrower’s bank account by $80,400.00

* Borrower was charged for the presence of an attorney when no one presented them

* High cost loan

* APR higher

* Borrower never received cash out as shown on HUD

* Borrower received no documents at closing

* Dual tracking (lender started to foreclose while working on a modification)

* Borrower never served foreclosure documents

* Foreclosure illegally started

* Bank took payments from borrower and than foreclosed

* Process server falsified documents stating they served borrower when they did not.

* No pre-foreclosure documents given to borrower

* Foreclosure filed during the 30 day and 90 period.

* Real Estate broker, mortgage broker and attorney worked together to obtain financing and sell property to an unsuspecting borrower providing him with false and misleading information

while also giving inaccurate and deceptive information to the lender.

The Making of a "Liar's Loan," With Help From The Loan Officer

What a shame that this type of behavior was allowed to exist and thrive.

http://www.dailyfinance.com/2011/01/18/making-a-liars-loan-with-help-from-the-loan-officer/?a_dgi=aolshare_twitter

http://www.dailyfinance.com/2011/01/18/making-a-liars-loan-with-help-from-the-loan-officer/?a_dgi=aolshare_twitter

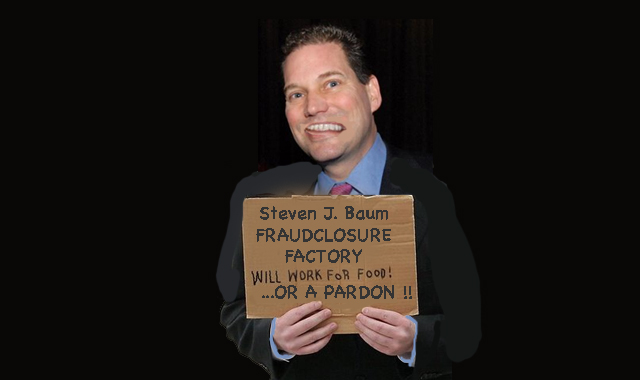

Newly Released Photo | Steven J. Baum Fraudclosure Factory “Will Work for Food! …Or a Pardon!!”

Baum, Baum, Baum....I guess the writing is truly on the wall. This is classic!

http://4closurefraud.org/2011/11/14/newly-released-photo-steven-j-baum-fraudclosure-factory-will-work-for-food-or-a-pardon/

http://4closurefraud.org/2011/11/14/newly-released-photo-steven-j-baum-fraudclosure-factory-will-work-for-food-or-a-pardon/

Monday, November 14, 2011

Fannie, Freddie CEOs Agree to Face Congress Over Bonuses this Wednesday

I can't wait to hear all of the crying and excuses.

You’re FIRED | Foreclosure Mill Lawyer Extraordinaire Steven J. Baum Dropped by Freddie Mac

Well it's a start! Cut off the rest of his cash flow and perhaps he'll close up on his own.

Superintendent Lawsky Announces Agreements With Morgan Stanley, Saxon, AHMSI & Vericrest On Groundbreaking New Mortgage Practices

If the banks made it a practice to hold their own paper, looked at borrowers as customers and not loan numbers and refrained from screwing their own customers these safeguards wouldn't be necessary.

http://www.dfs.ny.gov/about/press/pr1111101.htm

http://www.dfs.ny.gov/about/press/pr1111101.htm

Thursday, November 10, 2011

Elijah Cummings, the Homeowner Crusader

It's a shame that more of our elected officials don't step up to the plate like he has. Perhaps they should all personally experience foreclosure. Then I'm sure their tune will change.

http://www.politico.com/news/stories/1111/67715.html

http://www.politico.com/news/stories/1111/67715.html

Foreclosure law firm is battling rule on accuracy

New York ‘procedural hurdle’ called unconstitutional

Full Article:

Buffalonews.com

Wall Street, Main Street: Do You Have A Predatory or Fraudulent Mortgage?

Wall Street, Main Street: Do You Have A Predatory or Fraudulent Mortgage?: Do You Have Any Of These Violations On YOUR Mortgage?* Below you will find some of the results we have found after auditing our client’s m...

Florida Clerk of Court Sues Mortgage Electronic Registration System (MERS)

The lawsuit was filed by a county clerk in Florida which seeks class action status to represent the state’s 67 counties. The complaint claims the use of MERS does not comply with state property laws and has cost municipalities millions in unpaid recording fees.

The full story:

http://4closurefraud.org/2011/11/09/florida-clerk-of-court-not-sharon-bock-sues-mortgage-electronic-registration-system-mers-for-civil-conspiracy-unjust-enrichment-as-well-as-fraudulent-and-negligent-misrepresentation/

Re. Joe Walsh-Don't blame the banks

Hope he wasn't planning on being re-elected? Either, he's really misinformed or he's an idiot. You decide.

http://stopforeclosurefraud.com/2011/11/09/rep-joe-walsh-yells-at-his-constituents-dont-blame-the-banks/

http://stopforeclosurefraud.com/2011/11/09/rep-joe-walsh-yells-at-his-constituents-dont-blame-the-banks/

If you ever had any doubt the media is controlled . . . . . .

Hmmm. If this is true what are they making up about the housing market and foreclosures in general?

http://www.brasschecktv.com/videos/news-media-corruption/if-you-ever-had-any-doubt-the-media-is-controlled-.html

http://www.brasschecktv.com/videos/news-media-corruption/if-you-ever-had-any-doubt-the-media-is-controlled-.html

Americans Consider Housing Policy in 2012 Election

Housing, immigration, discriminatory (and unfair) taxes, extremely irresponsible gov't spending, incompetent and self-serving government, and on and on and on. ALL of this will end when the American people have had enough. We're beginning to wake up but we're not entirely there yet.

http://www.dsnews.com/articles/print-view/americans-consider-housing-policy-in-2012-election-2011-11-09

http://www.dsnews.com/articles/print-view/americans-consider-housing-policy-in-2012-election-2011-11-09

Wednesday, November 9, 2011

Lawmakers Want Answers on Bonuses to GSE Execs

The argument the GSEs have been promoting all along has been the need to keep pace with their private counterparts as it pertains to executive pay. Tighten your belt like everyone else. These "highly paid" executives are screwing everything up anyway. I say let the "rank and file" guys give it a go!

http://www.dsnews.com/articles/lawmakers-want-answers-on-bonuses-to-gse-execs-2011-11-08

http://www.dsnews.com/articles/lawmakers-want-answers-on-bonuses-to-gse-execs-2011-11-08

Tuesday, November 8, 2011

Palm Beach County Court Hosts Free Seminar - For Foreclosure Mills

Our tax dollars at work-- This is a start but Florida has a long way to go.....

Flyer Legal Staff Training5-1

http://www.foreclosurehamlet.org/profiles/blogs/outrageous-palm-beach-county-court-hosts-free-seminar-for

Flyer Legal Staff Training5-1

http://www.foreclosurehamlet.org/profiles/blogs/outrageous-palm-beach-county-court-hosts-free-seminar-for

New York courts brace for full force of foreclosure crisis

67% unrepresented by attorneys in 2011? Folks, here's a news flash. . . banks almost NEVER show up without an attorney. Do yourself a favor-find the best foreclosure defense attorney you can and hire them.

http://newsandinsight.thomsonreuters.com/Legal/News/2011/11_-_November/New_York_courts_brace_for_full_force_of_foreclosure_crisis/

http://newsandinsight.thomsonreuters.com/Legal/News/2011/11_-_November/New_York_courts_brace_for_full_force_of_foreclosure_crisis/

Policy Makers: Bank and Wall Street Greed, Not “Irresponsible Homeowners”, Caused Our Crisis

Wow, wow, wow! This is a MUST read (you must read the entire article to be fully disgusted). Again, if the general public did one thing these bankers do we'd go right to jail (no passing "go" , no "$200", no "get out of jail free card" for you). Honestly, when is enough enough?

http://4closurefraud.org/2011/11/08/abigail-field-policy-makers-bank-and-wall-street-greed-not-irresponsible-homeowners-caused-our-crisis/

http://4closurefraud.org/2011/11/08/abigail-field-policy-makers-bank-and-wall-street-greed-not-irresponsible-homeowners-caused-our-crisis/

Bank admits error after couple claims home was illegally taken

Way to go Chase! Because of the service this Vet gave to his country you should have immediately flown in an executive to handle the illegal foreclosure! The home owner had NO MORTGAGE on the property! God, what is wrong with you people?

http://www.conwaydailysun.com/node/476598/

http://www.conwaydailysun.com/node/476598/

Steven J. Baum | Rule Affirming Foreclosure Cases are Accurate is Unconstitutional

Baum, Baum, Baum. . . . . this guy has got to be kidding! Maybe he just isn't satisfied that everyone in N.Y. hates him. Maybe the goal is to have every living thing on the planet hate him. Does he really believe he has a shot here? Is he THAT delusional? If there ever were a time to make the insanity plea now is the time! Let us know how you feel!

http://4closurefraud.org/2011/11/08/steven-j-baum-rule-affirming-foreclosure-cases-are-accurate-is-unconstitutional/

http://4closurefraud.org/2011/11/08/steven-j-baum-rule-affirming-foreclosure-cases-are-accurate-is-unconstitutional/

Flaws Jeopardize New Attempt to Help Homeowners

Open Invitation To The Feds

This will NEVER work! It is beyond clear that the auditors are in bed with the banks. These "independent" auditors have either previous or current relationships with the banks. The Feds should hire their own auditors (and let the banks pay for the audits of course). If the Feds really want to get something done why don't you hire firms in the field (like us) who see predatory lending/servicing everyday?

http://www.propublica.org/article/flaws-jeopardize-new-attempt-to-help-homeowners

This will NEVER work! It is beyond clear that the auditors are in bed with the banks. These "independent" auditors have either previous or current relationships with the banks. The Feds should hire their own auditors (and let the banks pay for the audits of course). If the Feds really want to get something done why don't you hire firms in the field (like us) who see predatory lending/servicing everyday?

http://www.propublica.org/article/flaws-jeopardize-new-attempt-to-help-homeowners

Foreclosure Starts Rise as Servicers Process Backlog of Delinquent Loans

It would seem the backlog is due more to improperly filed paperwork than anything else (not to mention robo-signing).

http://www.dsnews.com/articles/print-view/foreclosure-starts-rise-as-servicers-work-through-backlog-of-delinquent-loans-2011-11-07

http://www.dsnews.com/articles/print-view/foreclosure-starts-rise-as-servicers-work-through-backlog-of-delinquent-loans-2011-11-07

Monday, November 7, 2011

Borrower Advocates Want Freeze on Foreclosures by Baum Law Firm

A homeowner defense organization has accused New York's largest foreclosure law firm of improper behavior and asked the state's top judge to discontinue any foreclosure cases the firm handles.

http://www.americanbanker.com/issues/176_215/foreclosure-defense-bar-baum-1043839-1.html

Sunday, November 6, 2011

A Must Read | The Collapse of Our Corrupt, Predatory, Pathological Financial System is Necessary and Positive

Great article! In order for us to get out from under this financial train wreck we need a solid foundation. The only way to accomplish that is to let everything hit rock bottom. Only from there can you start to rebuild.

CUMMINGS REQUESTS DOCUMENTS FROM LAW FIRM AFTER ALLEGATIONS OF FORECLOSURE ABUSE

http://stopforeclosurefraud.com/2011/11/05/cummings-requests-documents-from-law-firm-after-allegations-of-foreclosure-abuse/

Goldman Sachs Sued By Hedge Fund For Knowingly Selling Toxic Mortgage-Backed Investments

Anyone ever wonder how many former Goldman Sachs employees have gone to work for the White House? Am I the only one who sees a conflict here?

http://www.huffingtonpost.com/2011/10/28/basis-yield-alpha-fund-sues-goldman-sachs_n_1063762.html

http://www.huffingtonpost.com/2011/10/28/basis-yield-alpha-fund-sues-goldman-sachs_n_1063762.html

Freddie Mac Will Seek $6 Billion of Treasury Aid After Posting Wider Loss

A $6 billion (quarterly) LOSS!! It's NOT even for the whole year! Way to go! God these guys are good. Let's give them some more money!

http://news.businessweek.com/article.asp?documentKey=1376-LU33XX6K50XT01-4MG91POC9PRHEJTTKCGFIK1CFI

http://news.businessweek.com/article.asp?documentKey=1376-LU33XX6K50XT01-4MG91POC9PRHEJTTKCGFIK1CFI

HUGE Victory for Homeowners in the State of Florida – 2nd District Court of Appeals Issues Stunning Shot Across the Bow of US Financial Institutions

This was certain to happen. Folks, you couldn't make this stuff up if you tried!

http://4closurefraud.org/2010/02/13/florida-2nd-district-court-of-appeals/

http://4closurefraud.org/2010/02/13/florida-2nd-district-court-of-appeals/

House Members OCC FED Follow Up Letter on “Independent” Foreclosure Reviews

It sounds good but I don't see much happening here. Just a bunch of letter writing! Where's the big growling dog? Lenders will comply only when FORCED to do so.

http://4closurefraud.org/2011/11/04/house-members-occ-fed-follow-up-letter-on-independent-foreclosure-reviews/

http://4closurefraud.org/2011/11/04/house-members-occ-fed-follow-up-letter-on-independent-foreclosure-reviews/

DYLAN RATIGAN | NEVADA STATE ATTORNEY GENERAL CATHERINE CORTEZ MASTO FIGHTS FRAUDCLOSURE

Robo-siging a felony? $10,000 per offense? Sounds good to me!

http://4closurefraud.org/2011/11/03/dylan-ratigan-nevada-state-attorney-general-catherine-cortez-masto-fights-fraudclosure/

http://4closurefraud.org/2011/11/03/dylan-ratigan-nevada-state-attorney-general-catherine-cortez-masto-fights-fraudclosure/

Tammy Baldwin To Introduce Resolution Opposing Immunity For Banks In Foreclosure Deal

Again all of the investigations, threats and sanctions will not stop the banks from doing what they want to do. I believe only prison will do that.

http://www.huffingtonpost.com/2011/11/03/tammy-baldwin-immunity-banks-foreclosure_n_1072909.html?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+HP%2FPolitics+(Politics+on+The+Huffington+Post)

http://www.huffingtonpost.com/2011/11/03/tammy-baldwin-immunity-banks-foreclosure_n_1072909.html?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+HP%2FPolitics+(Politics+on+The+Huffington+Post)

Friday, November 4, 2011

Do You Have A Predatory or Fraudulent Mortgage?

Do You Have Any Of These Violations On YOUR Mortgage?*

Below you will find some of the results we have found after auditing our client’s mortgages:

Audited Results:

* Excessive fee charged to borrower $ 11,042.12

* Over compensation to mortgage broker $22,379.86

* Wrong lender foreclosing on borrower

* Borrower never received acceleration notice

* No HUD given to borrower at closing

* Mortgage broker over stated borrower’s income by $225,000.00

* Mortgage broker added false bank account to borrower’s loan application for $66,000

* Asset based lending

* Bait and switch. Borrower was switched at closing into an ARM loan

* No pre-closing documents – TIL, GFE, IOAF, Loan type, Broker’s fees

* Margin 7.125% (Adjustable rate loans only)

* TIL and Note payments do not match

* TIL does not clearly state mortgage payment

* Loan discount $ 9,315.00 – No benefit to borrower

* Mortgage broker never disclosed their additional fee of $4,627.00

* Mortgage broker promised borrower a cash out of $76,000 if they closed the loan.

* Borrower received no note at the closing

* Borrower never signed any closing documents. Broker “lifted” borrower’s signatures from a

previous loan.

* Mortgage broker closed loan at borrower’s place of business without an attorney, notary or

title company.

* Foreclosure filed during the 30 notice period

* Loan flipping. No benefit to borrower

* Closing costs ($75,966.65) higher than GFE ($47,377.15)

* $28,589.50 missing from closing (HUD)

* Hidden payment to mortgage by bank (YSP $17,402.16)

* Mortgage broker over stated borrower’s bank account by $80,400.00

* Borrower was charged for the presence of an attorney when no one presented them

* High cost loan

* APR higher

* Borrower never received cash out as shown on HUD

* Borrower received no documents at closing

* Dual tracking -

* Borrower never served foreclosure documents

* Foreclosure illegally started

* Bank took payments from borrower and than foreclosed

* Process server falsified documents stating they served borrower when they did not.

* No pre-foreclosure documents given to borrower

* Foreclosure filed during the 30 day and 90 period.

* Real Estate broker, mortgage broker and attorney worked together to obtain financing and

sell property to an unsuspecting borrower providing him with false and misleading information

while also giving inaccurate and deceptive information to the lender.

* The results shown above are the results from auditing the loans of both former and current clients. No guarantees can be offered or made as to the types, amounts or severity of violations that may be found on future audits.

CALL TODAY FOR A FREE CONSULTATION

Law Offices of Robert E. Brown, P.C

2409 Richmond Road, Staten Island, N.Y. 10306

Phone: 718-979-9779

Below you will find some of the results we have found after auditing our client’s mortgages:

Audited Results:

* Excessive fee charged to borrower $ 11,042.12

* Over compensation to mortgage broker $22,379.86

* Wrong lender foreclosing on borrower

* Borrower never received acceleration notice

* No HUD given to borrower at closing

* Mortgage broker over stated borrower’s income by $225,000.00

* Mortgage broker added false bank account to borrower’s loan application for $66,000

* Asset based lending

* Bait and switch. Borrower was switched at closing into an ARM loan

* No pre-closing documents – TIL, GFE, IOAF, Loan type, Broker’s fees

* Margin 7.125% (Adjustable rate loans only)

* TIL and Note payments do not match

* TIL does not clearly state mortgage payment

* Loan discount $ 9,315.00 – No benefit to borrower

* Mortgage broker never disclosed their additional fee of $4,627.00

* Mortgage broker promised borrower a cash out of $76,000 if they closed the loan.

* Borrower received no note at the closing

* Borrower never signed any closing documents. Broker “lifted” borrower’s signatures from a

previous loan.

* Mortgage broker closed loan at borrower’s place of business without an attorney, notary or

title company.

* Foreclosure filed during the 30 notice period

* Loan flipping. No benefit to borrower

* Closing costs ($75,966.65) higher than GFE ($47,377.15)

* $28,589.50 missing from closing (HUD)

* Hidden payment to mortgage by bank (YSP $17,402.16)

* Mortgage broker over stated borrower’s bank account by $80,400.00

* Borrower was charged for the presence of an attorney when no one presented them

* High cost loan

* APR higher

* Borrower never received cash out as shown on HUD

* Borrower received no documents at closing

* Dual tracking -

* Borrower never served foreclosure documents

* Foreclosure illegally started

* Bank took payments from borrower and than foreclosed

* Process server falsified documents stating they served borrower when they did not.

* No pre-foreclosure documents given to borrower

* Foreclosure filed during the 30 day and 90 period.

* Real Estate broker, mortgage broker and attorney worked together to obtain financing and

sell property to an unsuspecting borrower providing him with false and misleading information

while also giving inaccurate and deceptive information to the lender.

* The results shown above are the results from auditing the loans of both former and current clients. No guarantees can be offered or made as to the types, amounts or severity of violations that may be found on future audits.

CALL TODAY FOR A FREE CONSULTATION

Law Offices of Robert E. Brown, P.C

2409 Richmond Road, Staten Island, N.Y. 10306

Phone: 718-979-9779

Thursday, November 3, 2011

Fannie Mae, Freddie Mac executives get big housing bonuses

The Obama administration’s efforts to fix the housing crisis may have fallen well short of helping millions of distressed mortgage holders, but they have led to seven-figure paydays for some top executives at troubled mortgage giants Fannie Mae and Freddie Mac.

The Federal Housing Finance Agency, the government regulator for Fannie and Freddie, approved $12.79 million in bonus pay after 10 executives from the two government-sponsored corporations last year met modest performance targets tied to modifying mortgages in jeopardy of foreclosure.

The executives got the bonuses about two years after the federally backed mortgage giants received nearly $170 billion in taxpayer bailouts — and despite pledges by FHFA, the office tasked with keeping them solvent, that it would adjust the level of CEO-level pay after critics slammed huge compensation packages paid out to former Fannie Mae CEO Franklin Raines and others.

Securities and Exchange Commission documents show that Ed Haldeman, who announced last week that he is stepping down as Freddie Mac’s CEO, received a base salary of $900,000 last year yet took home an additional $2.3 million in bonus pay. Records show other Fannie and Freddie executives got similar Wall Street-style compensation packages; Fannie Mae CEO Michael Williams, for example, got $2.37 million in performance bonuses.

Including Haldeman, the top five officers at Freddie banked a combined $6.46 million in performance pay alone last year, though a second bonus installment for 2010 has yet to be reported to the SEC, according to agency records. Williams and others at Fannie pocketed $6.33 million in incentives for what SEC records describe as meeting the primary goal of providing “liquidity, stability and affordability” to the national market.

“Freddie Mac has done a considerable amount on behalf of the American taxpayers to support the housing finance market since entering into conservatorship,” Freddie spokesman Michael Cosgrove, told POLITICO on Monday. “We’re providing mortgage funding and continuous liquidity to the market. Together with Fannie Mae, we’ve funded the large majority of the nation’s residential loans. We’re insisting on responsible lending.”

A Fannie Mae spokesman said it is currently in a “quiet period” in advance of its third-quarter earnings report and declined to comment.

Most analysts believe the financial implosion of 2008 was fueled in part by Fannie Mae and Freddie Mac’s zeal in promoting homeownership and their backing of risky loans. And critics say that the mortgage giants’ deep backlog of repossessed homes, and their struggle through government conservatorship, is a staggering weight on a weak economy and puts even more downward pressure on home values.

“Fannie and Freddie executives are being paid millions to manage losses,” Rep. Patrick McHenry (R-N.C.), a longtime critic of the administration’s programs to rescue the housing market, told POLITICO. “By these same standards, I should be the starting forward for the Lakers. It’s completely absurd.”

“It is outrageous that senior executives at Fannie and Freddie are receiving multimillion-dollar compensation packages when they now rely on funding from U.S. taxpayers, many of whom face foreclosure or whose homes are underwater,” Rep. Elijah Cummings of Maryland, who has led House Democrats in efforts to ease Fannie and Freddie’s restrictions on restructuring loans or lowering payments for mortgage holders who owe more than their homes are worth, wrote in an email.

Compensation at Fannie and Freddie is, in fact, 40 percent below pre-government takeover levels, according to the FHFA, though those pay packages before conservatorship involved stock awards, while the current payments are exclusively cash. But compensation at both corporations, in particular Fannie Mae, has been a contentious issue since long before the 2008 financial meltdown, thanks to executives like Daniel Mudd, who earned $12.2 million in base pay and bonuses while heading Fannie, and Richard Syron, Freddie’s CEO, who pocketed $19.8 million in total compensation the year before the organization went into conservatorship.

- «Both Fannie and Freddie have long argued that they have to offer Wall Street-size paychecks to compete for the best private-sector talent. House Financial Services Committee Chairman Spencer Bachus (R-Ala.) introduced a bill in April to place the executives on a government pay scale, but it has yet to move out of committee.

FHFA’s acting director, Edward J. DeMarco, told Congress last year that the managers who were at the helms of the mortgage companies during the market collapse were dismissed but also argued that generous pay helps lure “experienced, qualified” executives able to manage upward of $5 trillion in mortgage holdings amid market turmoil.

DeMarco told lawmakers he’s concerned that suggestions to apply “a federal pay system to nonfederal employees” could put the companies in jeopardy of mismanagement and result in another taxpayer bailout. He said the compensation packages at Fannie and Freddie are part of the plan to return them to solvency while reducing costs to taxpayers.

A March report by FHFA’s inspector general, however, found the agency “lacks key controls necessary to monitor” executive compensation, nor has it developed written procedures for evaluating those packages.

An FHFA representative said the agency is installing pay package recommendations outlined in the report. Currently, she wrote, the agency “carefully reviews all executive officer pay requests and considers suitability and comparability with market practice, after consulting with the Treasury Department in certain circumstances.”

Since both companies’ stock is worthless, bonuses are paid in cash, deferred bonuses and incentive pay rather than stock options. A key factor in determining those bonuses is how Fannie and Freddie performed in the loan modification program created by the administration, in addition to measures tied to financial and accounting objectives.

For example, Freddie Mac helped a mere 160,000 homeowners change their mortgages “in support” of the president’s Home Affordable Modification Programand contacted only 45 percent of eligible borrowers, according to SEC filings. The company itself has modified 134,282 of its own loans since the start of the program. Those measures determined a significant share — 35 percent — of deferred bonus salary and, to a lesser extent, “target incentives” for Freddie executives.

Fannie, which was involved in modifying 400,000 mortgages last year, also assessed executive payments based in part on how it administered HAMP.

President Barack Obama in the past has derided Wall Street “fat cats” for raking in seven-figure bonuses even though their banks and finance companies needed billions of dollars in government bailouts just to stay in business. Yet the White House so far has remained largely silent about comparable bonuses at Fannie Mae and Freddie Mac.

The congressional criticism over compensation follows other charges that DeMarco has been unwilling to throw a lifeline to homeowners plunged underwater when the market collapsed.

The government-sponsored firms have essentially filled the vacuum caused by an exodus from private lenders. But critics want the FHFA to embrace “principal write-downs,” in which lenders and, by extension, Fannie and Freddie, would have to forgive a significant portion of homeowners’ outstanding mortgages; the move, they argue, would be a major step toward restoring housing market stability and boosting the economy but would force the two companies to accept red ink on their balance sheets.

DeMarco has resisted plans to modify troubled mortgages, insisting it wasn’t part of his legal mandate to bring Fannie and Freddie to fiscal stability.

Both HAMP and a similar program, Home Affordable Refinance Program, were seen as having the potential to modify at least 3 million government-backed mortgages and refinance 4 million others. The results were disappointing, however: Just 1.7 million borrowers have been helped since the programs were launched two years ago.

Last week, the White House announced a plan to relax restrictions for the HARP refinance program, which lets homeowners in good standing refinance their mortgages at current rock-bottom interest rates. DeMarco, whom aides say had been studying a similar proposal, gave the plan his blessing — a rare point of agreement between him and the Obama administration.

CORRECTION: An earlier version of this story incorrectly described the process by which the federal government took over Fannie Mae and Freddie Mac. They were both placed in conservatorship under the supervision of the Federal Housing Finance Agency.

“Worst Person of the Week” | Keith Olbermann Wears Guy Fawkes Mask While Giving Out Steven J. Baum’s Address (MUST VIEW VIDEO)

Be sure to watch the entire video…

“Steven J. Baum of Buffalo, NY is the state’s largest foreclosure mill,”

“It represents banks and mortgage servicers in their efforts to foreclose on homeowners and throw them out. It has been accused of trickery to try to evict people with steady incomes who were up to date on their mortgages. So naturally for Halloween, Steven J. Baum encouraged its employees — all of whom, I assume live in terror of becoming the next victims of their scumbag bosses — to dress up for homeless people, carrying bottles of booze, wearing signs that mock the excuse of those that have been unfairly evicted.”

Olbermann asked as the camera revealed him a Guy Fawkes mask.

“So this is what they dress up as for Halloween? We’re going to play that game, are we?”

Fawkes is a historical figure that has been adopted as a symbol of the hacker activist group “Anonymous.” The mask has recently been a favorite of protesters across the world.

And just like Anonymous might do, Olbermann disclosed the physical addresses of Steven J. Baum offices in Amherst and Long Island.

“It’s a long game, Steven J. Baum, and there are many costumes to be worn,”

“Being a foreclosure mill law firm is bad enough, adding visual abuse of your victims on Halloween, poor choice.”

Bank of America Forecloses on Home that does NOT Exist

The Law Offices of Robert E. Brown, P.C.

Bank Forecloses On Home Destroyed By Ike

HOUSTON — Hurricane Ike destroyed dozens of homes in Seabrook. Many families are just now rebuilding, but when Brad Gana tried to pick up the pieces, he learned that Bank of America was trying to take what little he had left.”

I was shocked when they said they were foreclosing on it,” Gana told investigator Amy Davis.

Gana was working overseas when the hurricane hit, destroying his home. But even then, he said he never missed a mortgage payment. It took him days to figure out why Bank of America was foreclosing.

“It wasn’t until about 20 calls that someone said, ‘We had a homeowner’s policy on your home that you reside in, and your monthly payments have gone up,’” Gana explained. “But they never notified me that my monthly payments had gone up.

“That’s right. Bank of America took out a forced homeowner’s policy on an empty slab.

You can check out the rest with video here…

United States of America v Allied Home Mortgage | Feds File Massive Fraud Case Against Allied Home Mortgage

The Law Offices of Robert E. Brown, P.C.

United States of America v Allied Home Mortgage | Feds File Massive Fraud Case Against Allied Home Mortgage

{kind=link}

Feds File Massive Fraud Case Against Allied Home Mortgage

by Tracy Weber and Charles Ornstein ProPublica,

Federal prosecutors sued Allied Home Mortgage Capital Corp. and two top executives Tuesday, accusing them of running a massive fraud scheme that cost the government at least $834 million in insurance claims on defaulted home loans.

Houston-based Allied and its founder and chief executive, Jim Hodge, were the subject of July 2010 stories by ProPublica [1], which detailed a trail of alleged misconduct, lawsuits and government sanctions spanning at least 18 states [2] and seven years. Borrowers recounted how they had been lied to by Allied employees, who in some cases had siphoned their loan proceeds for personal gain. Some lost their homes.

Despite years of warnings, the federal government had not — until this week — impaired the company’s ability to issue new mortgages.

The suit [3], filed Tuesday in U.S. District Court in Manhattan, seeks triple damages and civil penalties, which could total $2.5 billion. Simultaneously, the U.S. Department of Housing and Urban Development suspended the company and Hodge from issuing loans [4] backed by the Federal Housing Administration. The company was also barred from issuing mortgage-backed securities through the Government National Mortgage Association (Ginnie Mae).

Allied has billed itself as the nation’s largest privately held mortgage broker with some 200 branches. (At one point, the company operated more than 600.) The sprawling network made Hodge, a folksy Texan, a rich man [5] with properties in three states and St. Croix and two airplanes to get to them.

Allied and Hodge played the “lending industry equivalent of heads-I-win and tails-you-lose,” U.S. Attorney Preet Bharara said at a news conference Tuesday. “The losers here were American taxpayers and the thousands of families who faced foreclosure because they could not ultimately fulfill their obligations on mortgages that were doomed to fail.”

The government’s complaint alleges that between 2001 and 2010, Allied originated 112,324 home mortgages backed by the FHA, which typically go to moderate- and low-income borrowers. Of those, nearly 32 percent — 35,801 — defaulted, resulting in more than $834 million in insurance claims paid by HUD.

In 2006 and 2007, the company’s default rate was a “staggering” 55 percent, the complaint said.

In addition, another 2,509 mortgages are currently in default, which could result in another $363 million in insurance claims paid by HUD.

Borrowers told ProPublica last year that company employees falsified records to bolster their credit worthiness and lured them into unaffordable deals by lying about the terms.

The government’s complaint says: “Allied has profited for years as one of the nation’s largest FHA lenders by engaging in reckless mortgage lending, flouting the requirements of the FHA mortgage insurance program and repeatedly lying about its compliance.”

Tuesday’s action against Allied follows criticism that the government has been slow to act on rampant fraud and abuse in the mortgage market. In the case of Allied, the government had reams of evidence of possible misconduct. Among ProPublica’s findings last year:

- Allied had the highest serious delinquency rate [6] among the top 20 FHA loan originators from June 2008 through May 2010.

- Nine states sanctioned the firm from 2009 to mid-2010 for such violations as using unlicensed brokers and misleading a borrower.

- Federal agencies cited or settled with Allied or an affiliate at least six times since 2003 for overcharging clients, underpaying workers or other offenses.

- At least five lenders sued, claiming Allied tricked them into funding loans for unqualified buyers by falsifying documents and submitting grossly inflated appraisals, among other allegations.

Allied spokesman Joe James said the company was aware of the government lawsuit but had not received a copy of it and could not comment.

Hodge did not return a phone call and email seeking comment. But last year, he told ProPublica that the problems experienced at some of Allied’s branches should not tarnish his firm’s overall record. “If you look at the volume that we did or do,” he said, “it’s not significant.”

In an interview Tuesday, Helen Kanovsky, HUD’s general counsel, defended the time it took her department to take action.

“We had tried sanctions before,” she said. “We had assessed civil monetary penalties and that had not worked.

“The extraordinary remedy that we have — to be able to terminate somebody’s FHA capacity [and] basically put them out of business — requires a very high level of evidence and a high level of proof.”

The government’s 41-page lawsuit details an alleged scheme by Allied to deceive HUD about its employees and the risks associated with its loans. For years, it operated a network of “shadow” branches that were not approved by HUD and falsely certified that they met legal requirements.

Allied also disguised the high default rates of some branches, the complaint alleges, by tinkering with their addresses to apply for new HUD identification codes for the same offices. When HUD updated its system to prevent such manipulation, Allied simply moved all of its branches to a sister company and obtained new IDs, “thus again achieving a clean slate on its default rates,” the suit said. The sister firm, Allied Home Mortgage Corp., is also named as a defendant.

Hodge created a “culture of corruption,” the suit said. He “intimidated employees by spontaneous terminations and aggressive email monitoring, and silenced former employees by actual and threatened litigation against them.”

In one case, Hodge instructed his chief information officer to capture the password for the personal email account of Jeanne Stell, the company’s executive vice president and compliance officer. Then, he installed an electronic listening device under the information officer’s desk, the complaint alleges.

Allied also was employing felons, including a state manager who had been sentenced to 60 months in prison for distributing methamphetamine and a branch manager running the office under a falsely-assumed name, the suit said.

The government joined a whistleblower lawsuit filed by a former Allied branch manager in Massachusetts, Peter Belli. In addition to Allied and Hodge, the suit also names Stell as a defendant.

Belli had filed other suits against Hodge and Allied. He said Tuesday that, while his legal pursuit of his former employer had been long and hard, “I never really ever felt like quitting because I was married to the cause.”

Allied is also facing at least one federal criminal investigation into its now-shuttered Hammond, La., branch. In multiple lawsuits, borrowers allege that the office deceived them from 2005 through 2007 by misrepresenting loan terms, falsifying records, failing to pay off prior mortgages and diverting hundreds of thousands of dollars.

At his news conference, Bharara said Tuesday’s filing was a civil matter and that the investigation into Allied is continuing. “We will go wherever the facts lead us.”

Why the SEC Won't Hunt Big Dogs

"I was going to make a comment, but I think this one comment (in part) says everything" - John Brancato, Loss Mitigation Robert E. Brown, P.C. "I worked at the SEC HQ. I will tell you why this is all going on, because the SEC is the biggest revolving door for Government Attorneys. They work in Enforcement or Litigation for a few years and then rotate into a Securities firm doing Defense."

Note: The Trade is not subject to our Creative Commons license.

Back when the Financial Crisis Inquiry Commission [1] was doing its work, I would check in periodically with someone who worked there to find out how it was going.

"Good news!" my source would joke. "We got the guy who caused it."

In addition, the S.E.C. accused one person -- a low-level banker. Hooray, we finally got the guy who caused the financial crisis! The Occupy Wall Street protestors can now go home.

After years of lengthy investigations into collateralized debt obligations, the mortgage securities at the heart of the financial crisis, the S.E.C. has brought civil actions against only two small-time bankers. But compared with the Justice Department, the S.E.C. is the second coming of Eliot Ness. No major investment banker has been brought up on criminal charges stemming from the financial crisis.

To understand why that is so pathetic and -- worse -- corrupting, we need to briefly review what went on in C.D.O.'s in the years before the crisis. By 2006, legions of Wall Street bankers had turned C.D.O.'s into vehicles for their own personal enrichment, at the expense of their customers.

These bankers brought in savvy (and cynical) investors to buy pieces of the deals that they could not sell. These investors bet against the deals. Worse, they skewed the deals by exercising influence over what securities went into the C.D.O.'s, and they pushed for the worst possible stuff to be included.

The investment banks did not disclose any of this to the investors on the other side of the deals, or if they did, they slipped a vague, legalistic disclosure sentence into the middle of hundreds of pages of dense documentation. In the case brought last week, Citigroup was selling the deal, called Class V Funding III, while its own traders were filling it up with garbage and betting against it.

By the S.E.C.'s own investigations of and settlements with Goldman Sachs [3], JPMorgan Chase [4] and Citigroup, and by reporting like my ProPublica work with Jake Bernstein [5] and early [6] stories [7] by The Wall Street Journal, we know that these breaches were anything but isolated. This was the Wall Street business model. (Goldman, JPMorgan and Citigroup were all able to settle without admitting or denying anything, which, of course, is part of the problem.)

Neither the Citigroup settlement nor any of the others come close to matching the profits and bonuses that these banks generated in making these deals. And low-level bankers did not, and could not, act alone. They were not rogues, hiding things from their bosses.

Last week's S.E.C. complaint makes clear [8] that the low-level Citigroup banker that it sued, Brian H. Stoker, had multiple conversations with his superiors about the details of Class V. At one point, Mr. Stoker's boss pressed him to make sure that their group got "credit" for the profits on the short that was made by another group at the bank.

Pause, and think about that. The boss was looking for credit, but as far as the S.E.C. was concerned, he got no blame.

The S.E.C. did not respond to a request for comment, so we are left to wonder what explains its failure to reckon adequately with the pervasive problems. Contrary to expectations, the embattled and oft-assailed agency has done almost everything right with structured finance investigations, taking aim at abuses related to C.D.O.'s and other complex deals.

The S.E.C. has also devoted adequate resources to the issue. It put together a special task force on structured finance, sending the proper signal of the agency's priorities both internally and externally. The task force is staffed by bright people, an invigorating mix of young go-getters and experienced hands. Those people have understood for years what was wrong with the C.D.O. business on Wall Street.

O.K., so what is it? Risk aversion.

Based on the major cases the S.E.C. has brought, a pattern has emerged. It is making one settlement per firm and concentrating on only the safest, most airtight cases. The agency's yardstick seems to be, who wrote the stupidest e-mail? Mr. Stoker of Citigroup wrote an incriminating e-mail that recommended keeping one crucial participant in the dark. Goldman's Fabrice Tourre, the other functionary the agency has sued, wrote dumb things to his girlfriend.

But the S.E.C is not the G-mail G-man. It is the securities police. Imprudent e-mailing is not the only way to commit securities fraud.

Maybe the agency hopes that private litigation will take up the slack. It cannot investigate and wring a prosecution or settlement out of every corrupt deal. Instead, it has long aimed to plant a flag and let private litigants take care of the rest.

But private litigation has failed. One problem is that the defrauded institutions often committed their own sins. In a monstrous daisy chain, C.D.O.'s bought pieces of other C.D.O.'s. These investments were run by management companies. They might have been the victim in one C.D.O., but complicit in the predations of another.

Other victims, like large financial institutions and money managers, do not want to sue because it could reveal their own compromised behavior. Or they would be revealing to customers that they had simply been taken by other, smarter bankers. You cannot very well convince people that you are a good steward of their money if you are simultaneously complaining that the Wall Street sharpies fleeced you.

And private litigation has changed in the last decade and a half. The Private Securities Litigation Reform Act of 1995, which was meant to make class-action lawsuits harder to bring, has had a spillover effect beyond those cases, according to plaintiffs' lawyers. Courts have raised the bar for securities fraud cases, even where the act does not apply. The rules color how judges look at financial disputes.

So the S.E.C. has the wrong approach.

This is a matter of will and leadership. Its chairwoman, Mary L. Schapiro, while deserving credit for pushing investigations of structured investments, is sending the signal that she does not want to lose. Her agency is meekly willing to get token settlements when the situation calls for Old Testament justice.

Someday, the S.E.C. will have to go up against a top executive who has resources to fight, and who was too sophisticated to put anything rash in writing. This seems to be our fate: our bankers took reckless risks, but our regulators take none.

Subscribe to:

Posts (Atom)